Will Crypto Payments Kill Card Schemes?

Part I

The Numbers That Broke the Internet

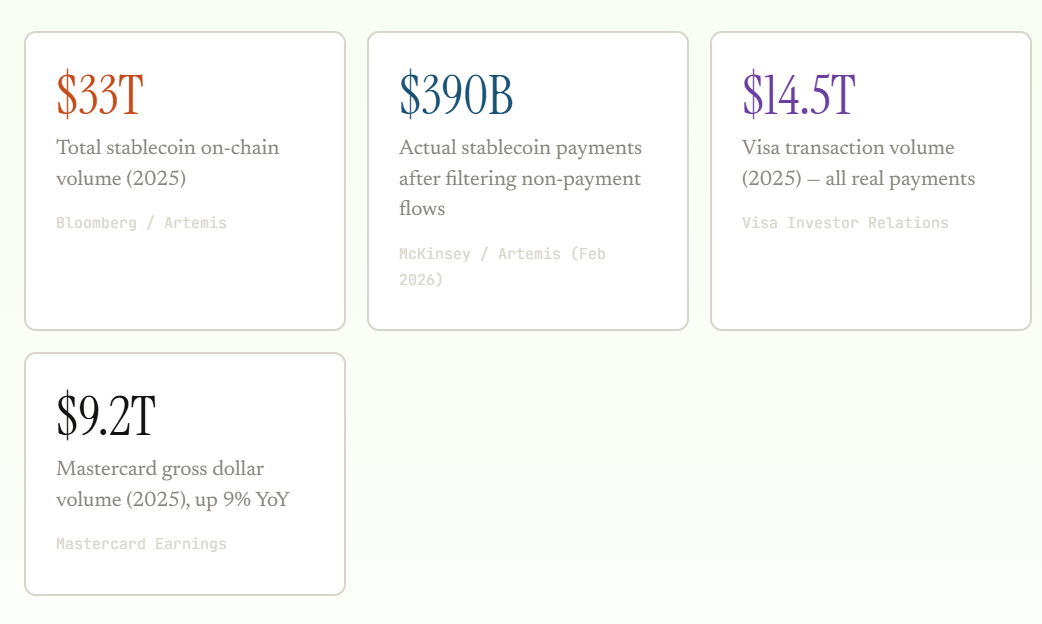

In January 2026, Bloomberg reported that global stablecoin transaction value totalled $33 trillion in 2025, up 72% from the prior year. USDC alone processed $18.3 trillion, surpassing Tether's $13.3 trillion.1 When placed next to Visa's $14.5 trillion in total transaction volume for the same year, it seemed like stablecoins had already won.2

But a McKinsey–Artemis Analytics joint analysis published in February 2026 punctured the narrative: the actual volume of real stablecoin payments — money exchanged for goods, services, salaries, and invoices — was roughly $390 billion, representing approximately 0.02% of global payments.3 The rest? Trading, DeFi recycling, liquidity provision, and internal treasury transfers.

The four major US card processors — Visa, Mastercard, American Express, and Discover — facilitated a combined $27.7 trillion in consumer transactions in 2024.4 With over 15 billion credit cards in circulation globally and acceptance at more than 150 million merchant locations, card networks operate at a scale that stablecoin rails have not remotely approached in actual payment terms.

Yet the growth trajectory is unmistakable. On an adjusted basis filtering out artificial activity, stablecoins processed about $9 trillion in transaction value over the past 12 months — up 87% year-over-year — according to Andreessen Horowitz's State of Crypto 2025 report.5 Monthly adjusted volume hit an all-time high of $1.25 trillion in September 2025 alone. Something real is happening. The question is: where exactly is it happening?

Part II

The Card Scheme Moats

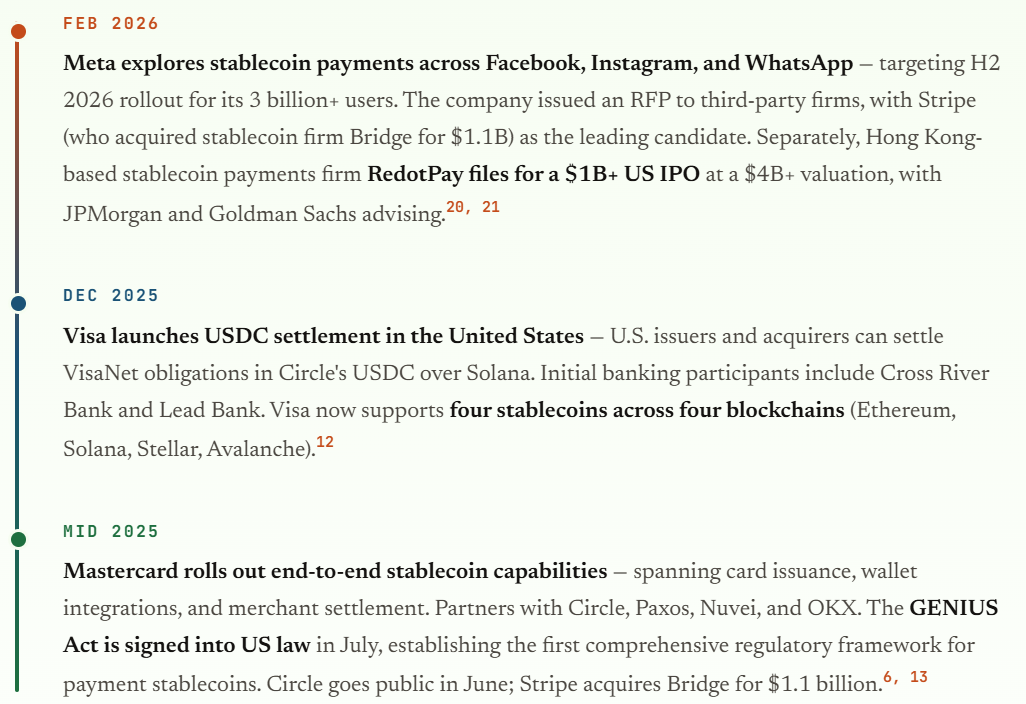

In their Q4 2025 earnings calls on January 30, 2026, both CEOs were blunt. Visa's Ryan McInerney stated plainly that in developed markets, consumers already have ample ways to pay with digital dollars — and that Visa sees "no product-market fit for stablecoin payments" in everyday consumer transactions.19 Mastercard CEO Michael Miebach echoed the sentiment, framing stablecoins as just "another currency" Mastercard can support within its network. Mastercard's Chief Product Officer Jorn Lambert had earlier noted that roughly 90% of current stablecoin volume goes toward trading in other cryptocurrencies, not general-purpose payments.6

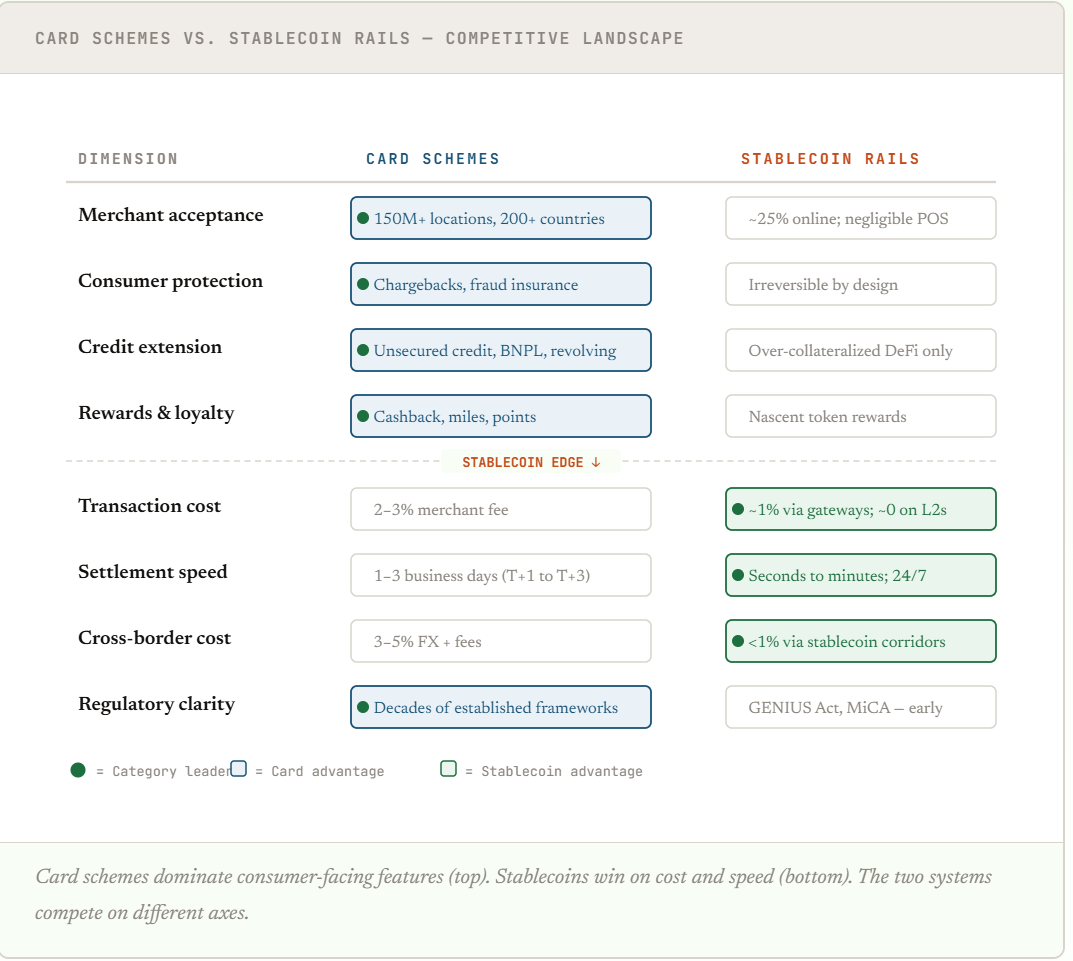

He's not entirely wrong. Card networks have built compounding advantages over more than seven decades that crypto rails cannot replicate overnight:

The network effect alone is staggering. Visa and Mastercard collectively control over 70% of global card market share, processing hundreds of billions of transactions per year across a fully mature ecosystem of issuing banks, acquiring banks, payment processors, and merchants.7 Rebuilding this from scratch — even with superior technology — takes years.

Perhaps the most overlooked moat is consumer behavior. A Paybis survey of 900+ users across the US, Canada, and Europe found that 47.6% still buy crypto with bank cards — compared to just 6.4% using Apple Pay and 4.6% using Google Pay.8 People trust what they know. And bank cards represent more than seven decades of trust.

Part III

Where Stablecoins Are Actually Winning

If $390 billion in real stablecoin payments sounds small next to $14.5 trillion, consider that it more than doubled from 2024 levels and that specific corridors are seeing explosive traction.3

B2B payments dominate

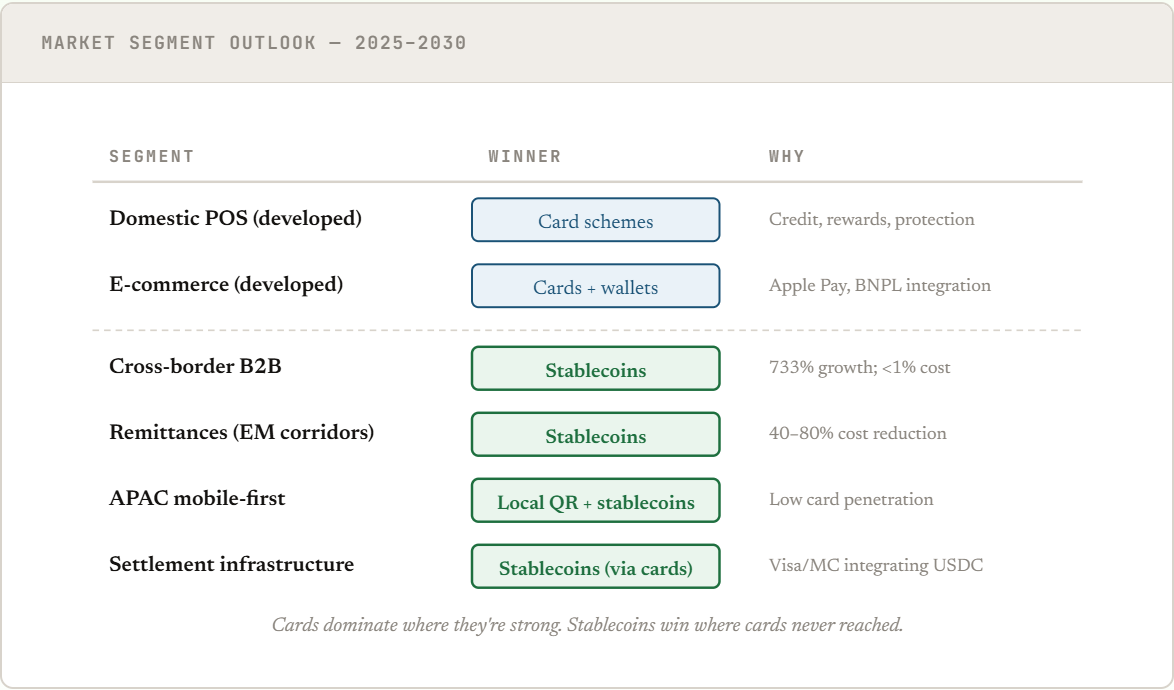

According to the McKinsey–Artemis analysis, B2B payments account for roughly $226 billion — about 60% — of global stablecoin payment volume. Year-over-year growth in B2B stablecoin flows was a staggering 733%.3 Import-export businesses in Latin America and Africa are integrating stablecoins into their payment operations, trading the friction of correspondent banking for instant, low-cost settlement.

Asia leads the charge

Stablecoin payments sent from Asia represent $245 billion — 60% of the global total, concentrated in Singapore, Hong Kong, and Japan.3 South Asia was the fastest-growing region for crypto adoption in 2025, with retail crypto transactions rising more than 125% between January and September compared to the same period in 2024.9

Cross-border remittances

This is where the value proposition is most visceral. Traditional remittance corridors still charge several percent on average globally. Blockchain-based transfers have demonstrated the ability to cut costs by 40–80% while settling in minutes rather than days.2 In Latin America, 71% of stablecoin activity is tied to cross-border payments — for remittances, inflation hedging, and commerce where traditional banking is limited.10

The crypto card bridge

Ironically, one of the fastest-growing crypto payment use cases rides on top of card rails. Crypto card volumes surged from ~$100 million monthly in early 2023 to over $1.5 billion by late 2025 — a 106% compound annual growth rate.11 Users hold stablecoins in their wallets but spend through Visa and Mastercard at existing merchant terminals. The consumer experience is unchanged; the settlement layer is transformed.

Visa now carries over 90% of on-chain crypto card volume, with stablecoin-linked card spend reaching a $3.5 billion annualized run rate by late 2025 — 460% year-over-year growth.11, 12

Part IV

The Convergence Thesis

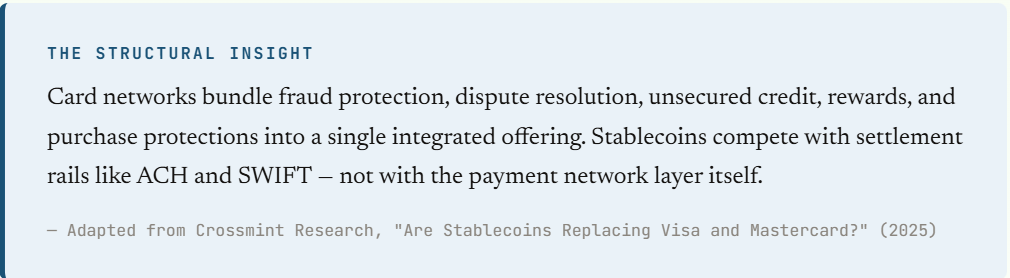

Here's the twist that most "crypto vs. cards" takes miss: the two systems are merging, not competing. Visa and Mastercard aren't fighting stablecoins — they're absorbing them.

The strategy is clear: card networks retain their consumer-facing value proposition — acceptance, protection, credit, rewards — while upgrading their settlement infrastructure from legacy correspondent banking to blockchain-based rails.

The irony is sharp: the same week Visa and Mastercard's CEOs told investors there was "no product-market fit" for stablecoins, Standard Chartered warned that stablecoins could draw up to $500 billion out of traditional bank deposits by 2028.22 And just weeks later, Meta — with 3 billion users — announced it was exploring stablecoin payments integration for H2 2026.20 If that happens, stablecoin payments won't need "product-market fit" — they'll have distribution at a scale that dwarfs every card network combined.

This is why BNP Paribas Equity Research concluded in 2025 that stablecoins do not currently have the potential to disrupt most domestic payment use cases — because debit cards already perform well on speed, cost, and access in developed markets. Where stablecoins shine is in cross-border corridors where the existing infrastructure is slowest and most expensive.14

Part V

The APAC Exception

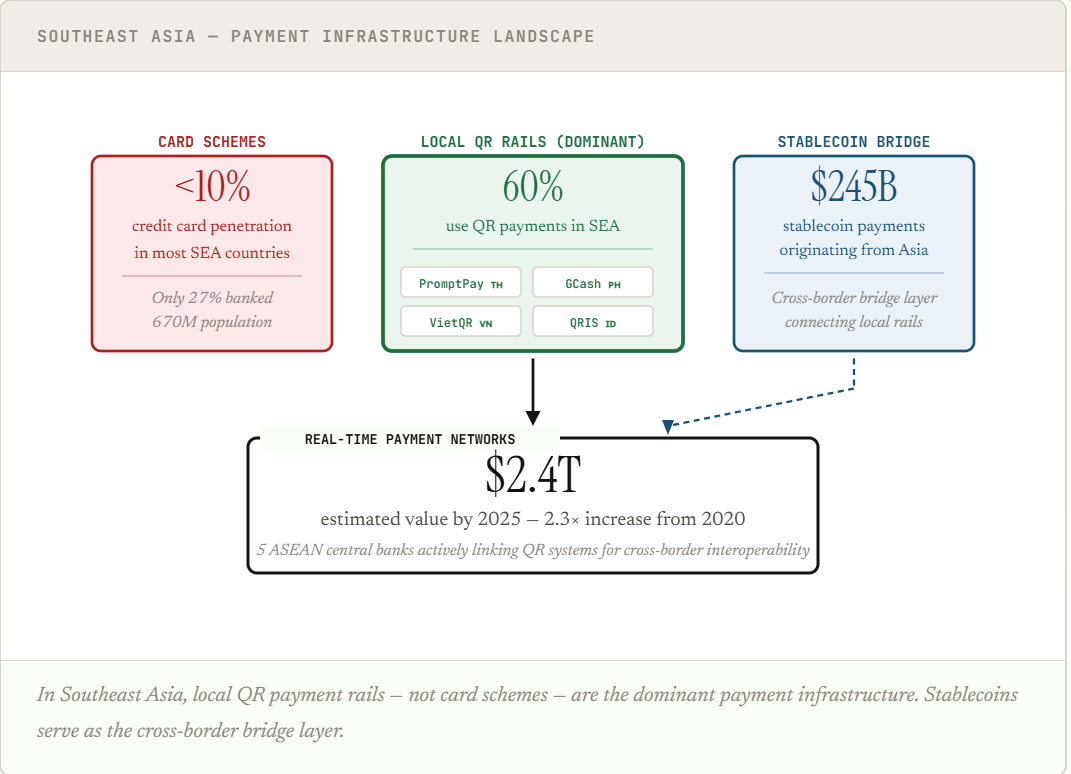

If the convergence thesis holds in developed markets, Southeast Asia tells a different story entirely. This is where card schemes were never dominant to begin with — and where alternative rails have a genuine chance to leapfrog them.

The numbers are striking: of the 670 million people in Southeast Asia, only about 27% have traditional bank accounts. Credit card penetration is below 10% in many countries.15 Yet smartphone penetration has outpaced banking, and QR-code-based payment systems have exploded. Nearly 60% of Southeast Asian respondents used QR payments as of 2022, and that figure has only risen since.16 Thailand's PromptPay processes around 50 million transactions per day. The Philippines' GCash serves over 81 million users.17

Real-time payment networks in Southeast Asia reached an estimated $2.4 trillion in value by 2025 — a 2.3× increase from 2020.18 And the five major ASEAN central banks — Indonesia, Malaysia, Philippines, Singapore, Thailand — are actively linking their QR payment systems for cross-border interoperability, bypassing the need for USD-denominated card networks entirely.

In this context, stablecoin infrastructure plays a complementary role. It doesn't compete with PromptPay or GCash for domestic transactions. Instead, it serves as the bridge layer between these local instant payment systems and global liquidity — enabling a Filipino worker in Singapore to send USDC that arrives as PHP in a GCash wallet within minutes.

This is the landscape where stablecoin payment orchestration becomes transformative — not as a replacement for cards, but as a protocol layer connecting stablecoin liquidity to the local banking rails that actually move money in APAC. The opportunity isn't to "kill" Visa. It's to serve the corridors and populations that Visa was never built to reach.

Verdict

Sources & References

- Bloomberg / Artemis Analytics — "Stablecoin Transactions Soared 72% in 2025, Hit $33T" (Jan 2026)

- CoinLaw — "Global Payment Network Statistics 2025" citing Visa $14.5T volume, Mastercard $9.2T GDV

- McKinsey & Company / Artemis Analytics — "Stablecoins in Payments: What the Raw Transaction Numbers Miss" (Feb 2026)

- Capital One Shopping — "Credit Card Market Share (2025)" citing $27.7T combined US processor volume

- Andreessen Horowitz (a16z) — "State of Crypto 2025" report, $9T adjusted stablecoin volume

- Payments Dive — "Mastercard, Visa Play Down Stablecoin Threat" (Jul 2025)

- Market Report Analytics — "Credit Card Networks Market Expansion: Growth Outlook 2025–2033"

- Paybis / FinanceFeeds — "Why Bank Cards Still Dominate Crypto Purchases in 2025" (Dec 2025)

- TRM Labs — "2025 Crypto Adoption and Stablecoin Usage Report"

- CoinLedger — "Stablecoin Market Share and Transaction Volume" (Sep 2025 data)

- Artemis Analytics — "Stablecoin Payments at Scale" (Jan 2026)

- Visa Inc. — "Visa Launches Stablecoin Settlement in the United States" (Dec 16, 2025)

- BNP Paribas CIB — "Stablecoins – A New Payments Revolution?" (Oct 2025)

- BNP Paribas Equity Research — Stablecoin payment disruption assessment (2025)

- HitPay — "Alternative Payment Methods in Southeast Asia" (May 2025)

- CSIS — "Your Card Has Been Declined: Realignment of SEA's Digital Finance Ecosystem" (2025)

- The Fintech Times / Paymentology — "Asia Pacific's Digital Finance Revolution" (Oct 2025)

- Nium — "How APAC is Winning the Real-Time Payments Race" (Sep 2025)

- CoinDesk — "Visa and Mastercard Aren't Buying the Stablecoin Hype" (Jan 30, 2026)

- CoinDesk / Bloomberg — "Meta Is Planning Stablecoin Comeback" (Feb 24, 2026)

- Bloomberg / PYMNTS — "RedotPay Is Said to Consider $1 Billion US IPO" (Feb 24, 2026)

- Crypto News Australia — Standard Chartered $500B deposit flight warning (Feb 2, 2026)